Taxes are complicated, especially in the cannabis industry.

Between state, county, and municipal/local government regulations, cannabis tax rates are approaching nearly 50% in some areas.

California is arguably the largest and most diverse legal cannabis market in the world. The state is divided into 58 counties and 482 incorporated cities and towns. By law, each of these territories is permitted to determine its own cannabis policies and taxes in addition to the state regulations. That’s why you’ll find different tax rates when shopping in Los Angeles compared to San Diego, San Francisco, or Oakland. With so many hands in the tax revenue pot (pun intended), taxes are even more convoluted for cannabis businesses in California.

If you're opening a dispensary in California, or looking for help with your current retail operation, this quick guide outlines the basics of how and when taxes are charged for medical and adult-use marijuana retailers in California—as well as cannabis point-of-sale features in Flowhub that make setting up taxes for your dispensary easy.

For specific taxation requirements for other license types, please refer to the California Department of Tax and Fee Administration (CDTFA) Tax Guide for Cannabis Businesses.

California cannabis excise taxes

By definition, an excise tax is a tax incurred mid-supply chain between a supplier that provides a manufactured cannabis product and its final retail destination where it is sold to the consumer.

Because there are several license types, and therefore business models that exist in California, it is important to understand the difference between when and how excise tax collections occur. Here is a quick breakdown:

Arm’s length - retailers licenses

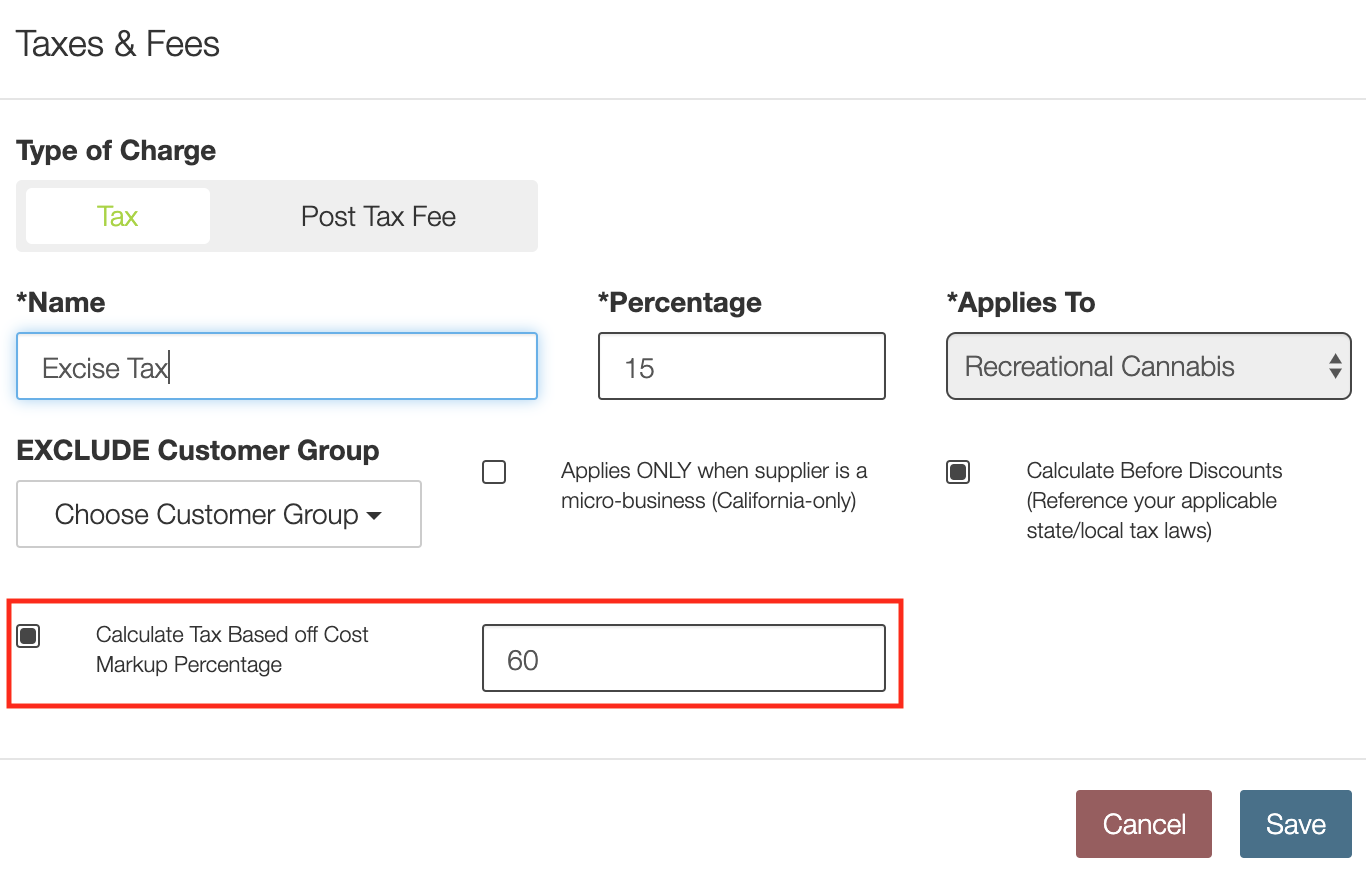

For retail licenses that are not their own suppliers who buy products from a licensed third-party and separate business entity, the excise tax is paid on what is defined as an “arm’s length transaction”. This means that the retailer pays for the excise tax when purchasing products from a supplier (a.k.a. wholesale purchase). The amount of that tax is included in the sales price for the customer, which includes the markup percentage from the wholesale cost and does not need to be calculated again during the retail sale. Effective January 1, 2018, a 15 percent excise tax is imposed upon every cannabis purchase in California. In an arm’s length transaction, this 15 percent tax is calculated based on the “cannabis excise tax mark-up rate” set by the California Department of Tax and Fee Administration or CDTFA every 6 months. The cannabis excise tax mark-up rate is currently set to a 60% markup of a retailer’s wholesale cost. Wholesale cost includes transportation charges and any discounts or trade allowances.

Setting up excise tax markup calculations in Flowhub

To set up your excise tax markup calculations correctly in Flowhub, first navigate to Manage > Location Management > and then choose Taxes & Fees from the drop-down selection at the top of the screen. From here, click the plus icon in the top right-hand corner to add this tax markup calculation. Below is an example of how an excise tax calculation would be set up with Flowhub. Keep in mind that the cannabis excise tax markup rate changes every 6 months, and the below numbers are merely an example. Please refer to the CDTFA for the most up-to-date information about the current excise tax rate, and cannabis excise tax mark-up rate.

Non-arm’s length - microbusiness licenses

Microbusiness licenses have the option of being completely vertically integrated, meaning these licensed cannabis businesses can operate as their own producer, manufacturer, distributor and therefore supplier of their cannabis retail operation. When the goods being sold are manufactured by a directly related licensed entity, this is known as a “non-arm’s length transaction”, and the excise tax is passed along directly to the consumer at the time of the retail sale. If a microbusiness also sells products manufactured by a third party and completely separate business entity, the non-arm’s length excise tax does not apply to those specific products.

Setting up arm’s length and non-arm’s length cannabis taxes in Flowhub

Flowhub makes it easy to delineate between arm's length and non-arm's length suppliers so taxes can be calculated correctly, no matter what products the customer purchases. Managers use Flowhub's product catalog to create a database of suppliers. If the supplier is a related business entity or vertically integrated with the retailer, the manager simply clicks a checkbox as seen in the image below.

What are cumulative cannabis taxes?

In California, there are sometimes two, three or even four separate taxes applied that are charged at the point of sale. These taxes include excise taxes, sales taxes, municipal or local business taxes, and any additional flat fees. Unlike other states that calculate taxes just on the simple subtotal or retail price of an item, California and Michigan marijuana taxes must be calculated with a certain order of operations to arrive at the correct total, as the taxable amount increases and compounds after each tax is calculated. We call this type of layered calculation “cumulative taxes” or “compounding taxes”.

For an in-depth explanation on how these cannabis taxes are calculated, please refer to: How to Calculate Cannabis at Your Dispensary.

Setting up cumulative taxes for CA in Flowhub

Flowhub gives cannabis retailers flexibility and granular control over how taxes are calculated. Because cannabis taxes in California are cumulative, they must follow a specific order to reach the correct total. In Flowhub, California retailers can set up each tax as a ‘step’ that succeeds another to build a complete tax profile. For example, a 15 percent excise tax must be calculated first, followed by sales tax second, then proceeded by local taxes third.

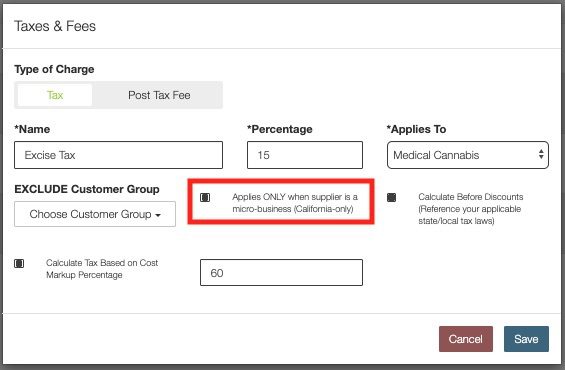

As discussed earlier, this Flowhub tax profile is where non-arm’s length taxes are set up and calculated first for all products. If the retailer has a microbusiness license and supplies some of their own inventory, a non-arm’s length excise tax will need to be set up and for both medical and recreational cannabis products, so that the charge for this tax will be directly passed on at the point of sale to the consumer.

Flowhub makes the delineation very easy by indicating that this tax applies only when the supplier is a connected microbusiness in California. For example, in the screenshot below we’ve set the excise tax for medical products to apply ONLY when the supplier is a microbusiness.

Calculating California cannabis taxes on the gross receipt

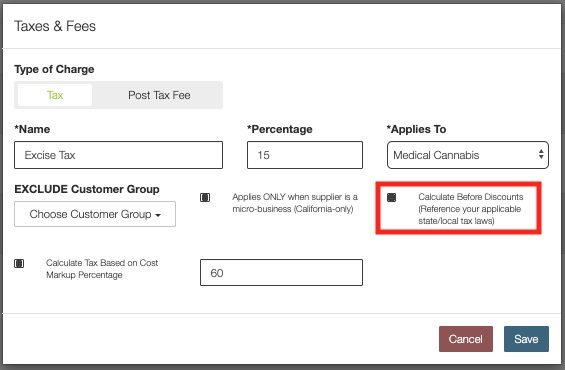

There are additional factors that make cannabis taxes in California unique compared to other regulated states. In most other markets, taxes are applied to the subtotal of all products being purchased after discounts are applied. The Bureau of Cannabis Control (BCC) has decided to maximize state tax revenue from cannabis sales by requiring that taxes be applied on ‘Gross Receipt’ or the price of each item before discounts.

Flowhub cannabis point of sale puts the control in your hands by allowing dispensaries to calculate taxes before discounts are applied. If you are in California, Nevada or Michigan, click the box to 'Calculate Before Discounts' and Flowhub will automatically do the math for you and make sure you collect taxes compliantly and correctly.

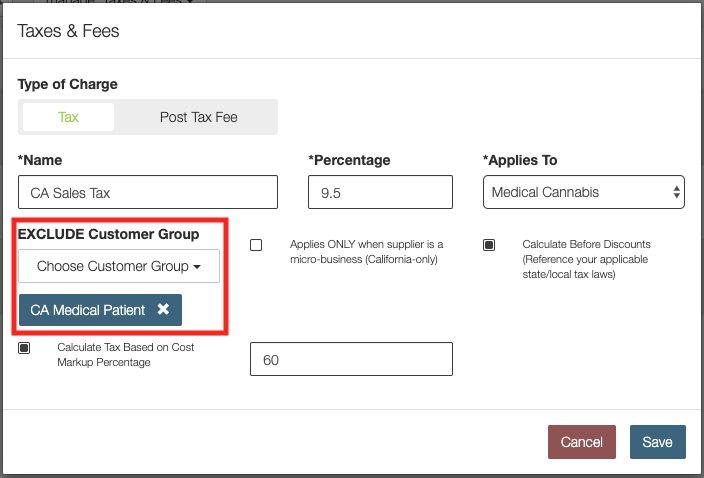

Did you know? California medical patients are sales tax exempt

To make California taxes even more complicated, medical patients with a valid state-issued medical marijuana identification card are not required to pay state sales tax on their medicine. You can ensure that no verified California medical patient gets charged sales tax by following a few simple steps in Flowhub.

First, be sure to your Customer Groups are set up correctly within Flowhub.

To exclude sales tax for patients with a valid California medical marijuana identification card, simply select the correct customer group from the drop-down options under ‘EXCLUDE Customer Group’ when setting up the sales tax. Check that all other fields are correct, then hit ‘Save’.

Please note that this tax still applies to California Medical Patients that do not have an official medical marijuana identification card, even if they have other temporary documentation and are in the process of getting their official state-issued medical card.

Cover your bases for tax compliance

Collecting taxes correctly is a huge part of running a fully compliant retail marijuana business. When evaluating your options for technology partners, remember to ask the hard questions. Find out exactly how your chosen point-of-sale provider helps you with all the unique regulations associated with California taxes and makes tax compliance easier.

If you want to see these features in action, watch a demo today. Or give us a call directly at (844) FLOWHUB to quickly get your questions answered by a team member.