Dispensary Payments

The 2026 Guide to Cannabis Payment Processing Solutions

This post was first published in April 2020 and updated in February 2025 to address the current state of cannabis payments.

The cannabis boom is gaining momentum. The US cannabis industry is expected to reach almost $45 billion in revenue in 2025.

Federal initiatives like descheduling of cannabis or the SAFE Banking Act would also have a considerable impact on the industry.

In 2025, there's a big opportunity for new or expanding marijuana dispensaries—if you can do it well.

Roadblocks remain, with one of the biggest questions still being... Why can’t people use credit cards to pay for cannabis?

In this age of convenience—constant connection, one-click purchase, fast and free delivery—consumers expect hassle-free payment options, no matter what they’re buying.

But cannabis isn’t like every other industry.

In this guide, we’ll explain how to get cannabis payments right.

First, you’ll learn about the cannabis payment processing services currently available, including why you can't take credit cards. Then, you’ll see how accepting debit or ATM cards can positively impact your business.

Finally, we’ll outline the future of cannabis payments and steps you can take to get started with accepting payment methods in your dispensary today, including how to choose a trusted payments partner.

Read on for the full guide, or click the links on the left to jump to a section.

Current cannabis industry payment options

Dispensaries have relatively few choices for processing cannabis payments.

Here are your most likely options and some considerations with each, plus our take on the best option for marijuana payment processing available today.

Cash

Cash is the most widely available and direct payment method. But only accepting cash comes with other considerations and limitations.

Being "cash-only" limits your ability to upsell customers because cart sizes are limited to the cash someone has in their pocket.

Physical cash also presents a logistical and security challenge. Collection at the point of sale becomes more prone to mistakes and inaccuracies as humans are responsible for counting and processing thousands of dollars in cash every single day.

Closing the books at the end of the day is also more complicated, as managers will have to revisit every transaction to figure out discrepancies. Plus, transactions are also slower when you need to count cash and supply change.

Most impactfully, having cash around significantly increases security concerns and costs to transport cash. Dispensaries looking to deposit their daily or weekly earnings need to have large and costly vaults and armored vehicles to protect their money. Armed robbery and internal theft are running rampant in the cannabis industry with criminals attracted to large stockpiles of cash. The more cash you have, the more you risk losing.

While having an ATM in-store mitigates a few of these concerns, they often carry hefty fees, take up floor space, and create a disjointed check out experience for customers. Even if you own your store's ATM and collect revenue from the fees, you're still losing out on significant revenue due to workflow errors and spending limitations.

If you’re planning to have cannabis delivery/ecommerce at your dispensary, you’ll also have to contend with the fact that drivers might end up carrying around thousands of dollars in cash on a daily basis. This puts them and your revenue at risk.

Beyond security and logistical cash management considerations, there’s also a component of personal safety. Cash is dirty. A physical dollar bill can carry pathogens and disease. This is another reason why there’s a renewed desire for touchless, mobile ways to pay for cannabis products.

Read this next

18 Cash Management Tips for Cannabis Retailers

Despite the risks of being a cash-only business, it’s an unavoidable reality. Even if you offer other forms of payment, some people will still use cash so make sure you understand best practices for dispensary cash management and have rock-solid SOPs for dispensary safety and security.

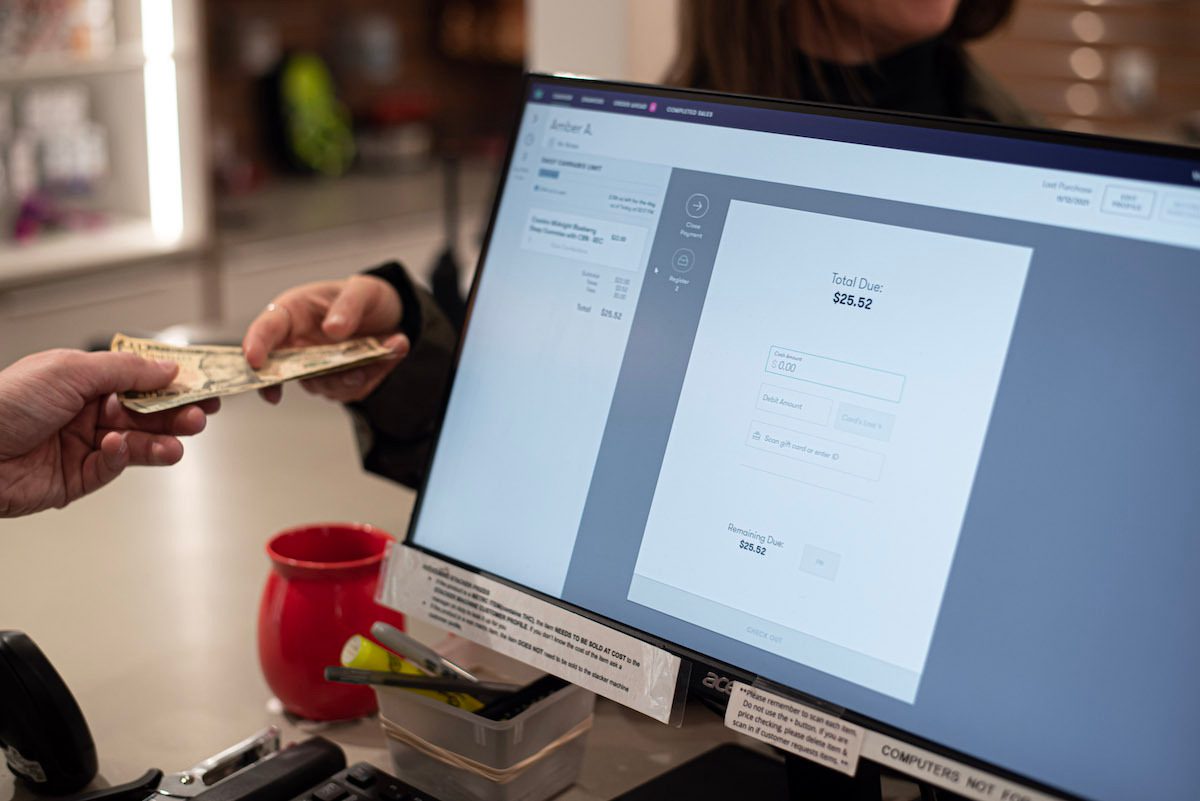

Point of banking (POB)

Point of banking has become more common in cannabis but is rarely used in other industries. (Note: some people call this "cashless ATM", but that term isn't widely accepted or recognized. "Point of banking" is the more legal terminology).

Point of banking is a payment method that allows the customer to access their bank account at the point of sale.

Point of banking functions similarly to traditional ATMs, where a customer inserts a debit card and enters their personal identification number (PIN).

Because point of banking is actually an ATM transaction at the point of sale, customers generally have to pay in increments of $5, although some solutions can round to the nearest $1. If a transaction doesn’t come out to a round number, the budtender has to return the difference in change (which tends to increase tips).

Additionally, consumers are charged a convenience fee on top of the rounded total. The processing fee amount varies depending on the merchant. Some point of banking vendors offer a portion of this fee back to cannabis retailers in the form of a rebate.

This process—especially when it’s integrated with your point of sale—feels like a traditional debit card transaction for customers and streamlines checkout for dispensaries. Beware of non-integrated cannabis payments solutions, they can cost you thousands.

Point of banking has emerged as the most stable middle ground for cannabis businesses because it’s reliable, widely-used, increases basket size, satisfies customers, and has the benefit of being a touchless transaction.

If you’re using a standalone, non-integrated reader, the budtender will need to key in the amount before the consumer runs their card. This sounds simple, but the chance of human error is significant. It's important to go with an integrated option to ensure long-term success.

Be aware: Not all point of banking solutions are created equal. Any cannabis payment processor that claims to be entirely cashless is not compliant for cannabis. The solution may be in violation of network rules and is at risk of being shut down.

Before choosing a point of banking provider, triple-check that they are compliant and network rules are being followed.

ACH transfers

Another viable cannabis payment option is to accept electronic funds transfers from bank accounts.

This digital payment process facilitates transfers through ACH (Automated Clearing House) and refers to the process of transferring money between banks without checks, wire transfers, or cards.

Since these transfers are electronic, businesses can immediately verify that the funds exist and go directly from the customer's account to your bank account. ACH or bank transfers are simple, secure, legal, and reliable.

The challenge with accepting ACH payments from your customers is the need for third-party solutions. With these, customers have to first register through the third-party system in order to make payments at your dispensary.

For a seamless customer experience, your POS should be integrated with your ACH payment solution. In this instance, the customer simply scans a QR code to pay.

You can enable ACH payments today with the Flowhub and Aeropay integration.

PIN Debit

Traditional PIN debit cards may seem like a viable option because, on the surface, they are similar to point of banking (both use a bank card).

But debit transactions run on a different “rail” or payment network. This payment rail is the same one credit card processing runs on, which is not ok for cannabis (more on that in a second).

You read that right: traditional debit card processing is not ok for cannabis.

With PIN debit, you can only pay with the money you have available in your account. It's an instant charge and covers payment to the exact penny. So many people think debit is a compliant way to pay for marijuana products, but it's risky.

Some merchant services have even attempted to disguise cannabis debit transactions as charges for items like pet toys or purchases at nearby businesses. Scams like this do not go unnoticed and can lead to arrests and indictments.

👉 Learn the risks of PIN debit!

Credit cards

Credit card payments are what cannabis consumers are asking for. Paying by card is easy for the customer to understand since they’re used for 28% of all payments across industries.

83% of Americans between 30 and 49 years old own a credit card. Most consumers prefer card payments (either debit or credit) over cash and only 10% make all their purchases with cash. It’s obvious why dispensary owners are desperate to accept cards.

But dispensaries cannot accept credit card payments. The unfortunate fact is that the federal-level illegality of cannabis prevents credit payment processors, like Visa, Mastercard, or AMEX from knowingly participating with any marijuana businesses.

You or a cannabis retailer you know may have been impacted by a sudden shutdown of their dispensary's credit card processor. That's because it's a regular occurrence, leaving retailers high and dry without a compliant system.

The fact is, dispensaries simply cannot accept credit cards. Credit card processors won’t work with cannabis businesses. Period. If anyone is claiming otherwise and offering you a solution, you should turn it down as it could expose your business to legal risks.

This is why traditional card processing isn't a compliant option.

The federal stance on cannabis will need to change dramatically before credit card companies recognize us as a valid, legal form of business.

Still, some dispensaries are taking the risk and accepting credit cards as a workaround because they are desperate to accept other forms of payments.

It can be tempting to accept credit cards, even as a stop-gap measure, but it could be a business-ending mistake. We’ll go into more detail on the risk of credit card processing in cannabis in the next section.

Cryptocurrencies

The future is digital, right? Using crypto as a payment solution in your dispensary seems like a win — it's all digital, anonymous, and seemingly secure.

Some have even said crypto could save the cannabis industry. It's true that the two concepts align quite well in theory. Cryptocurrencies could solve the banking and payments problems in cannabis. But the volatility and risk associated with cryptocurrency make it an unrealistic option for cannabis retailers.

Perhaps someday there will be a reliable, easy-to-use, and industry-wide cryptocurrency for cannabis. The truth is we’re still far from that reality. Only a handful of stores have gotten this tech up and running, and none are operating regular transactions through crypto.

The bottom line is it’s too early to rely on cryptocurrency as a primary cannabis payment solution.

Takeaway: Point of banking or ACH

The best current options for cannabis payment processing are compliant point of banking solutions and ACH.

As of now, these are the safest, most reliable, and most consumer-friendly solutions for seamless payments.

Consumers want an easy way to pay and dispensaries want to be able to accept multiple forms of payment.

The risk of credit card processing in cannabis

We’re still in the Wild West of cannabis right now, which might lead some to believe that anything goes. Perhaps you’ve considered using credit card processing — an appealing option many will tell you is safe. We’re not trying to spread unnecessary fear, but you need to be aware of the risks.

You may be looking for payment solutions, even temporary gap options until federal legalization allows other solutions, but credit card processing at your dispensary puts your business in jeopardy, even in the short-term.

Here’s a scenario that continues to play out across the country: A dispensary starts accepting credit cards through traditional retail credit card processing avenues and experiences significant sales increases. A few weeks in, they get a knock on their door, or more likely, an email alert or phone call. In some cases, it’s the credit card company shutting down their merchant account. Seems harmless, but in doing that, they can also freeze all credit card payments processed the previous day (because they hadn’t yet been fully processed and transferred to the cannabis merchant account).

Even though cannabis is legal in many states, credit card companies still won’t work with cannabis businesses or other industries they consider “high-risk.”

They have built algorithms to flag transactions or merchants selling cannabis. They may not identify you immediately, but they will eventually.

It’s not just the loss of the prior day's revenue and shutting down the merchant account that’s the problem, it’s that your merchant account will be blacklisted. Thinking ahead, this could mean that you aren’t allowed to accept credit cards even when the rest of the industry is.

The risk of accepting credit cards isn’t limited to the card company. The state may also get involved; inquiring why your business is not compliant with their regulations. Sometimes, it’s both. Those weeks of missing income can easily end a young company, and running afoul of regulations can mean a lost license. Just like that, a dispensary could be out of business.

Takeaway: Think long-term

While it’s tempting to turn to credit cards, it’s worth handling payments by the books from the start. The risk (shutdown, loss of profit, loss of license) is simply not worth the reward.

The benefit of payments on marijuana-related businesses

Just selling cannabis doesn’t make a dispensary successful anymore — customers and patients have choices and high expectations.

Dispensaries need to differentiate on customer experience, and that includes an easy checkout experience.

Just a quick look at keywords on Google shows that consumers are actively looking for dispensaries near them that take cards. Having a point of banking or digital bank-to-bank (ACH) solution will instantly separate you from the competition.

The best part? Cash-free payments can increase revenues and satisfy customers with little to no cost to you.

In fact, we’ve found that average cart size increases by 30% on average with alternative payment options. When customers aren’t limited by the cash they have in their pocket, they’re more likely to browse for additional products and make last second additions to their cart.

Read next

See how Greatest Hits increased cart size 31% with integrated payments

Budtenders are also better equipped to upsell customers without added spending limits.

All in all, point of banking and ACH provide a better customer experience, meaning shoppers are more likely to return to your store. And for you, the retailer, enabling all these solutions also makes it easier to run your business.

Here's the proof: Data found that the average cash transaction (across all transactions and industries) is $22. However, the average non-cash (or card) transaction is $112. That’s a huge difference.

Greatest Hits in Massachusetts saw a 31% increase in average cart size when they started using integrated point of banking.

To maximize the positive business impact, look for an integrated solution. Integrated means that the cannabis transactions process within your point of sale software (rather than being a separate process where you manually key in the amount).

Integration reduces human error and automates accounting, which cuts down on administrative work and manager reconciliation.

Takeaway: Details matter

Customer experience is an important factor in the competitive landscape of cannabis dispensaries. Integrated point of banking and ACH solutions make for the smoothest shopping experience and make consumers more likely to give you even more of their business.

The future of cannabis payment processing

It may seem like adult-use and medical marijuana payment options are limited (because they are). However, the future of payments will be different. Cannabis companies can look to onboard new payment solutions and begin coaching their customers to actually adopt the digital payment solution.

As legislative action on cannabis picks up around the United States, and federal government officials talk about cannabis banking solutions, the tipping point may be coming.

Federal authorities are watching the scales tip and legislative easing around federal-level financial services for the cannabis industry is already on the table.

But that doesn't mean banking and payment processing will suddenly be easy for the cannabis industry. Even with new legislation, banking will still be a challenge.

Here’s what you need to keep your eye on:

SAFE Banking Act

This act would allow the major financial institutions to become fully involved in legal cannabis sales without fear of federal action or penalty. The SAFE Banking Act has passed the U.S. House of Representatives seven times. Previously, the SAFE Banking Act passed the House by a vote of 321 to 101. Now, it's pending in the Senate Committee on Banking, Housing, and Urban Affairs,. However, the domino effect of state-level legalization and Biden’s promise to reschedule the cannabis plant will make a difference in the coming months/years.

Learn moreReclassification of Schedule I status

The reclassification of cannabis’s Schedule I status has been a legal issue since 1972. A change in cannabis scheduling would be significant for the marijuana industry and would help unlock traditional banking services. The Drug Enforcement Administration (DEA) proposed rescheduling cannabis from Schedule I to Schedule III of the Controlled Substances Act (CSA) on May 21, 2024. This would reclassify cannabis as a drug with a moderate to low potential for dependence, and would allow it to be used for medical purposes.

Learn more280E

This specific section of federal tax code effectively prevents any cannabis seller or producer from ever claiming business expenses to reduce taxable income. Various cases have been tried around 280E, setting the precedent for certain company structures that avoid the disadvantages of this rule. The best way to deal with this is simple: find a great accountant who is familiar with the cannabis industry and has the experience you need. As cannabis becomes a more and more legitimized (not to mention extremely profitable) industry, we predict this specific rule will come under increasing scrutiny.

Learn moreTakeaway: Regulations are changing

Things are changing, slowly but surely. In the meantime, navigating all these rules can be a huge headache, especially for someone new to the space or new to small business ownership. Lean on partners to help you build your business and give customers what they want without taking on unnecessary risks. If you’ve got a strong foundation, this evolution will be much easier for your business to take on.

How to choose a payment processing vendor

Before adopting any cannabis payment option, be sure to thoroughly vet the solution, the vendor, and the cannabis payment contract. The payment processing oligopoly has become predatory.

Here are areas to watch:

Contract terms - Many providers will lock you into long-term contracts with expensive early termination fees. Look for vendors with flexible agreements, no exclusivity rights and no early cancellation fees.

Fees - Look for partners with transparent pricing and fees. Some payment providers will charge additional fees to the dispensary such as monthly statement and platform access fees, annual compliance fees, decline fees, support fees, termination fees, etc.

Integration - Using a non-integrated solution increases the risk of human error and reconciliation challenges. Seek a partner with an existing built-in integration with your point of sale solution to relieve yourself of operational hassles.

Frequently asked cannabis payments questions

Can dispensaries accept credit cards?

Even though cannabis is legal in many states, credit card companies still won’t work with cannabis businesses or other industries they consider “high-risk.” As long as cannabis is federally illegal, credit cards will not be a compliant payment option for cannabis dispensaries.

Can cannabis dispensaries accept crypto?

In theory, cannabis dispensaries can accept cryptocurrency payments, but we’re still far from that reality. Only a handful of stores have gotten the proper technology up and running, and the uncertainty surrounding the financial future of cryptocurrencies is still a risk. For the time being, crypto is not a viable payment option for cannabis businesses.

How to get started with cannabis payment processing

Dispensary owners and managers are looking for ways to streamline their businesses, grow profits, and satisfy customers. The answer is in cannabis payments, specifically point of banking or ACH.

These options give you the most flexibility to adapt as the market changes. Schedule a demo with Flowhub to learn more!

Disclaimer: Flowhub is not in any manner providing legal services or legal advice. You are solely responsible for consulting with legal counsel to ensure your business complies with all applicable laws, and we recommend you do so.