Most new industries start out fragmented and consolidate as competition increases and consumer needs mature. This is true in sectors like auto manufacturing, fitness, and tobacco, where each is dominated by a small number of large firms.

Today, the legal cannabis market is trending in the same direction.

This post addresses the state of consolidation in cannabis retail with expert insight on the market as M&A deals ramp up.

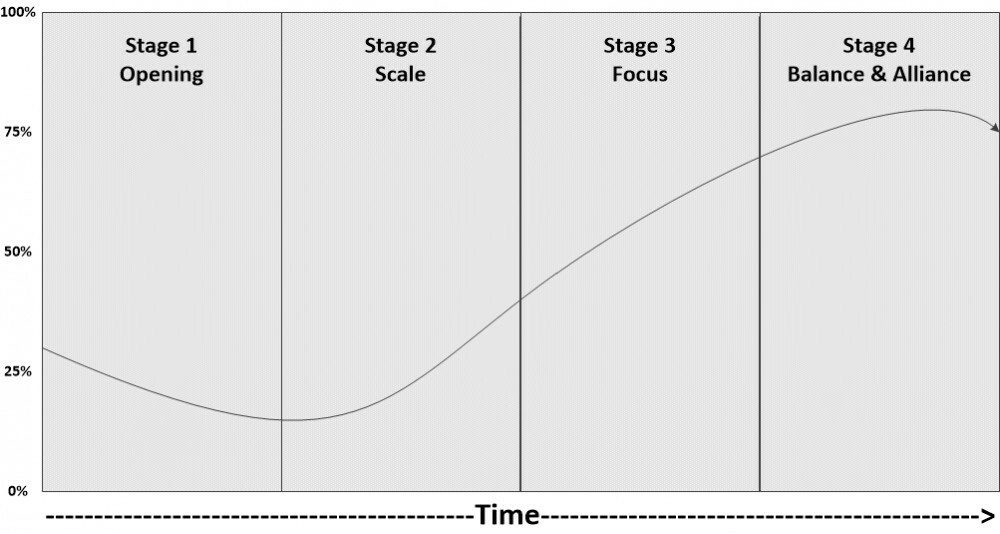

The consolidation curve

In the early ‘00s, global management consulting firm Kearney analyzed almost 2000 M&A deals and discovered a phenomenon they called “The Consolidation Curve”.

The firm laid out a four-step consolidation path that all industries go through:

Opening

Scale

Focus

Balance & Alliance

According to the curve, the cannabis industry is currently in the Scale stage, which involves considerable M&A, enabling the larger players to capture more market share as the smaller ones drop off.

The cannabis industry's path through the Scale stage is complicated by extensive regulations, siloed regional supply chains, and limited access to capital. All of these stand in the way of M&A deals that would typically be fervent during this period.

These challenges are reflected in 2022's deal volume, which was down 80% from the previous year.

Viridian Capital Partners logged just $3.2 billion in M&A deals in 2022, down from $10.3 billion the previous year. The deals were relatively small (unlike previous years, not a single deal closed over $500M) and many proposed acquisitions hit the rocks as interest rates rose and SAFE banking failed to make it through congress once more.

The right way to look at cannabis M&A

Many industry players think M&A activity will continue to be sluggish in 2023. The combination of a cash crunch, high interest rates and continued regulatory uncertainty are expected to work against potential acquirers.

“I think it’s going to be a very cautious market,” said Roxanne Peyser, Partner at Fortis Law, a Colorado-based law firm with a cannabis practice specializing in M&A.

“We’re seeing a number of large companies withdrawing from deals or kicking the can down the road,” she adds, pointing to failed deals like Ascend’s proposed acquisition of MedMen’s New York assets and Verano pulling out of a deal with Goodness Growth, a Minnesota-based multistate operator.

But Peyser believes the right way to look at the cannabis M&A landscape is regional.

She sees that valuations and activity in western states declining on account of slower growth and crashing wholesale prices while eastern and limited license states continue to show promise.

This outlook is in line with the emerging trend that newly legal markets outperform mature markets. In 2022, the three oldest cannabis markets (Colorado, Oregon, and Washington) all saw large sales retractions.

As 2023 heats up, expect to see more new money heading East, while consolidation heats up in the West.

A green opportunity, for the right price

While the East’s cannabis market shines bright, the flip side is that depressed valuations in the mature Western states are causing some entrepreneurs to try to cut their losses and look for the exit, creating opportunities for more cavalier buyers.

David Kram, an investment banker with a decade of deal-making in the cannabis industry under his belt, thinks this is the perfect environment for buyers with access to capital and the stomach to endure uncertainty.

Given the depressed valuations of dispensaries and other assets across the industry, it’s a better time than ever to be looking at acquisitions of retail licenses. The prices are the lowest they've ever been and operators across the country are struggling and looking to throw in the towel.

David Kram, Cannabis M&A and Capital Advisory

In this environment, the market has become saturated with distressed assets pushing prices down and a lack of cash on the buyer side has changed the structure of deals. (Viridian reported that just $5.9 million in funding closed in the first three weeks of 2023, compared to $157.2 million in the same period last year.)

“In the past, they might have been paid 50 percent or more in cash, but we're not going to see that anymore,” notes Peyser. “The structure of the buyout is going to be some combination of note and stock, possibly with some cash.”

We’re seeing these very deals Peyser alludes to already, like the recent combination of The Parent Company and Gold Flora in an all-stock deal. The combined company, called New Parent, is expected to streamline operations and generate annualized savings of $20 million and $25 million.

The ‘phantom number’ phenomenon

While buyers might be able to use the leverage of struggling businesses to their advantage, they are working against what Kram describes as “phantom numbers”.

Phantom numbers are valuations that sellers' assets had when they entered the industry. These perceived values are often much higher than what the business is worth today.

“What's really making M&A deals hard right now is that sellers are still emotionally attached to the perceived value they put on their business years ago,” adds Kram. “Sellers need to come to terms with the reality of the market. The days when you could sell your dispensary for $20M are gone.”

Phantom numbers also play a part in the unreasonable business practices that some dispensaries come to market with, such as exorbitant store layouts and lackadaisical operational practices. The expectation that legal cannabis is a get-rich-quick scheme is not warranted in the face of scaling competition, hefty taxes, and congressional gridlock.

Some cannabis retailers will continue clinging to their businesses and perceived valuations as long as the promise of regulatory changes, such as SAFE banking and federal legalization hang over the horizon.

But others will be left with no choice but to jump ship and cut their losses — leaving considerable opportunity for larger operators to swoop in and expand.

Will cannabis mirror the fitness industry?

For indications about what consolidation in cannabis might look like in the long run, we can draw parallels with other industries, like fitness, which was largely birthed in the 80s and consolidated in the 90s.

In an interview with mg magazine, veteran fitness and hospitality consultants turned cannabis advisers, Bob Thomas and Jim Snow, highlight the similarities and give cannabis operators a sense of what to expect in the coming years.

“Many of these first-to-market fitness clubs made millions of dollars even in subpar locations. The industry became known for poor service, weak operations, and shady business practices,” said Snow. “What we’re seeing in cannabis is there’s a little bit of corporate structure starting to seep in, but the industry, on the whole, is primarily independent, individually owned stores and operations. That’s where the fitness industry was [before consolidation began].”

Private equity’s involvement in the fitness industry through companies like Gold’s and 24 Hour Fitness sped up consolidation, and it will likely play a considerable role in doing so with cannabis too. While it’s expected to take the passing of SAFE Banking to usher PE firms into the industry en masse, there is some evidence that the attractive valuations are luring them in early.

BNN Bloomberg reported private equity firms will be a driving force in cannabis M&A this year. They are nicely positioned to come into legal markets in both Canada and the U.S., sweep up assets and implement a roll-up strategy.

But as much as the public MSOs and Wall St like to insist that cannabis is “just another CPG category” and the plant just another commodity, quality product from craft producers matters in mature markets.

Whether the major companies like it or not, cannabis retains some of its counter-cultural roots. The recent retreat of Curaleaf from the competitive Western markets of Oregon, California, and Colorado suggests that just because you’re big doesn’t mean customers will choose your business.

The impact of Federal legalization

Federal legalization continues to loom as a catalyst for the cannabis industry. It’s the point at which valuations are expected to skyrocket and opportunities to uplist on the US exchanges will open up vast amounts of retail investor capital for public companies.

“I think that by the time federal prohibition ends, consolidation will have already occurred,” says Peyser.

Viridian’s recent report on M&A highlighted that the “six largest U.S. MSOs combined accounted for approximately $5.0B (20 percent) of cannabis industry revenue in 2021” and that no single operator had as much as 5 percent market share. Small private companies with average revenue of $1.6M, on the other hand, accounted for over 60 percent of total industry sales. This, Viridian feels, is evidence that the majority of M&A is still in front of us.

As federal legalization nears, the necessary scale of cannabis businesses required to compete will increase. “The industry is capital-intensive, and tremendous sums will need to be spent to establish national brands, distribution systems, and centralized production facilities.”

We anticipate a wave of consolidation as companies seek to position themselves to achieve economies of scale in production, marketing, and logistics that are not yet available in the state regulatory regimes. As in the beer industry, there will always be thousands of craft cannabis companies, but the share of revenues earned by the largest competitors is likely to double over the next five years.

Frank Colombo, Director of Data Analytics at Viridian Capital Advisors

Are you a cannabis retailer considering a merger or acquisition for your company? I'd love to hear your perspective on the opportunity and potential pitfalls in the world of cannabis M&A. Connect with me on Linkedin.